-

Puregen Labs Meclizine

1 × $$55.00

Puregen Labs Meclizine

1 × $$55.00

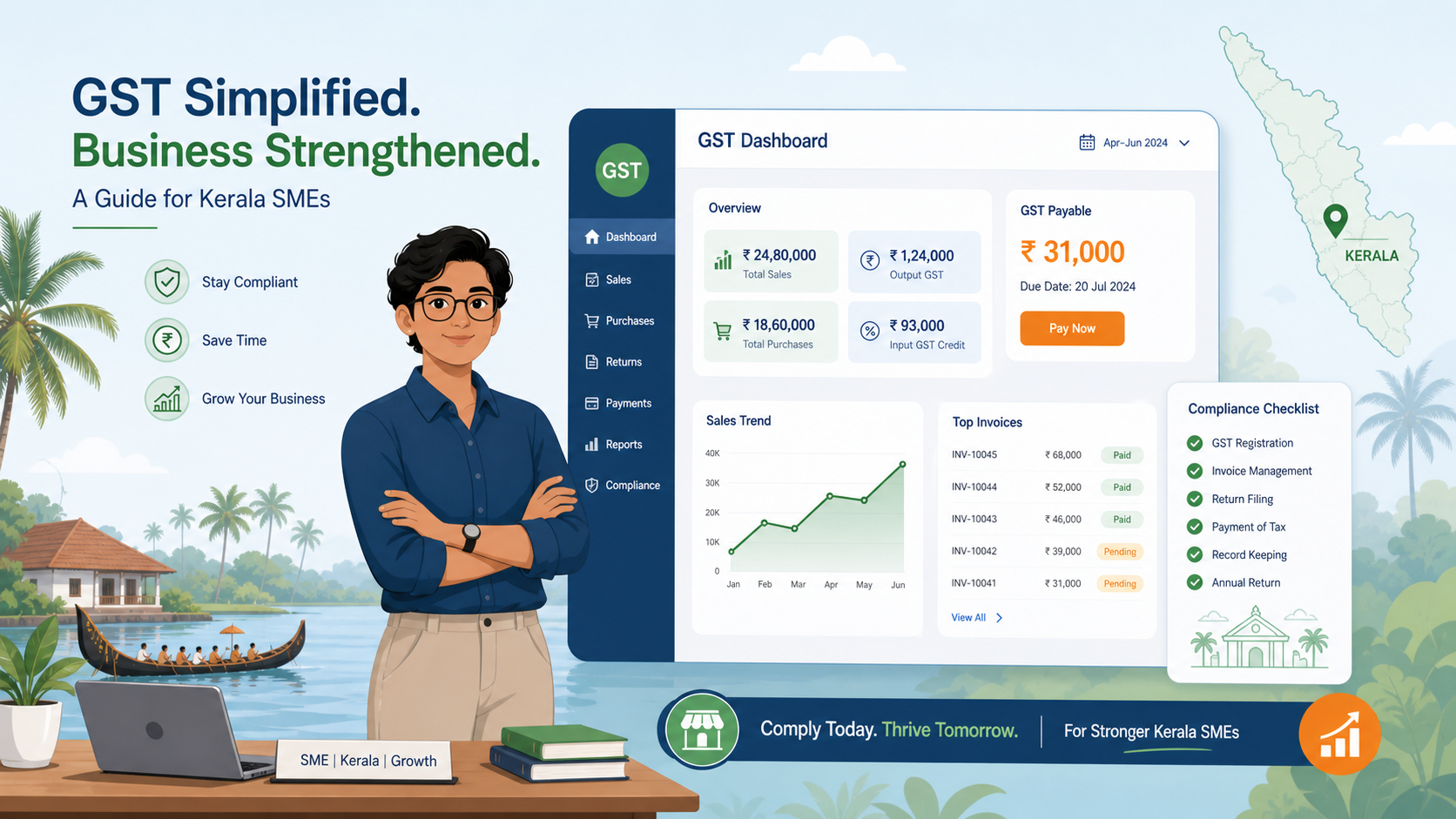

Stop Treating GST Like a Tax Problem — A Kerala SME Roadmap

May 19, 2026

49 views

Most Kerala SMEs treat GST as just another tax burden — but that mindset is costing them time, money, and growth opportunities. This blog by MACS Edge reframes GST as a business management tool rather than a compliance headache. It offers a practical roadmap for Kerala's small and medium enterprises to move beyond reactive filing and instead use GST structures — like Input Tax Credit optimisation, composition scheme selection, and return reconciliation — to strengthen cash flow and reduce risk. Whether you're a startup or an established business, this guide helps you take control of your GST compliance with clarity and confidence.

The Opening Argument

Most SME owners think GST is a tax problem. It is not. It is a cash-flow, credibility, and credit-rating problem disguised as a tax problem. Owners who treat GST as a quarterly nuisance lose working capital to blocked Input Tax Credit, lose B2B customers to vendor-compliance scoring, and lose bank limits because their filing history reads poorly. Owners who treat GST as a discipline win on all three. This note is about the strategic choices — not the button-clicking.

1. The Registration Decision — Strategy, Not Procedure

Kerala is a normal-category state, so the thresholds are Rs. 40 lakh for goods and Rs. 20 lakh for services. But the threshold is the least interesting part of the decision. The real questions an SME owner should be asking are:

- Who is your customer? If a significant share of revenue is B2B, voluntary registration below threshold often makes sense — corporate buyers will demand an invoice that carries ITC, or they will switch vendors.

- Are inter-state sales, marketplace sales, or exports on the horizon? Then the threshold is irrelevant — registration is compulsory from rupee one.

- Is the business in a 100% exempt line? Then registration is not required at any turnover. Many businesses register out of fear and lock themselves into a regime they did not need.

- Is the business building toward a bank limit, an MSME loan, or a tender empanelment? A clean 24-month GST history is increasingly a silent eligibility filter for institutional credit.

Registration is not a compliance event. It is a market-positioning decision.

2. Picking the Right Filing Regime — The Real Choice Matrix

Once registered, the strategic call is which lane to sit in. Kerala SMEs typically fit one of four:

| Lane | Best For | Hidden Cost |

|---|---|---|

| Regular Monthly | Turnover above Rs. 5 crore, B2B-heavy, exporters | Roughly 25 filings a year, full ITC machinery, e-invoicing above Rs. 5 crore |

| QRMP | Turnover up to Rs. 5 crore, mixed B2B/B2C | Tax still paid monthly; only paperwork is quarterly — frequently misunderstood |

| Composition (Goods) | Turnover up to Rs. 1.5 crore, B2C, intra-state | No ITC, no inter-state outward supply, no major e-commerce platforms |

| Composition (Services 10(2A)) | Services up to Rs. 50 lakh | 6% flat — requires careful margin math |

The lane should be reviewed every 31st March. Staying in a lane out of habit is one of the costliest forms of inertia in GST.

3. The Compliance Calendar — What to Diary, Not What to Do

An SME owner does not need to know how to file. They need to know which dates trigger consequences if missed.

| Anchor Date | What's Due | Who It Hits |

|---|---|---|

| 11th monthly | GSTR-1 | Regular monthly filers |

| 14th monthly | GSTR-2B reconciliation (internal) | All regular filers |

| 18th quarterly | CMP-08 (tax payment) | Composition dealers |

| 20th / 22nd monthly | GSTR-3B | Regular / QRMP (Kerala = Group B = 22nd) |

| 25th of M1 & M2 | PMT-06 tax challan | QRMP |

| 31st March | LUT renewal, scheme switch, vendor cleanup | Exporters and all regular filers |

| 30th June | GSTR-4 (annual) | Composition dealers |

| November 3B | Last-call ITC for previous FY | All regular filers |

| 31st December | GSTR-9 / 9C | Turnover above Rs. 2 crore / Rs. 5 crore |

Of these, the 14th monthly and the November cut-off are the two most under-appreciated dates in the SME boardroom. The 14th is when vendor failures get exposed. November is when the door closes on recovering that ITC.

4. The Composition Scheme — Underused, Misunderstood, Sometimes Mis-sold

Eligible SMEs can opt in at:

- Rs. 1.5 crore for goods, manufacturers, and non-alcohol restaurants — 1% or 5% rates.

- Rs. 50 lakh for services and mixed suppliers under Section 10(2A) — 6% flat.

- Plus a service allowance of 10% of turnover or Rs. 5 lakh, whichever is higher, for goods dealers.

When Composition is the Right Call

- Pure B2C profile — retail, food service, personal services, small-format establishments.

- High value-addition with low-GST inputs, so foregone ITC is small.

- Intra-state operations only, no marketplace dependency.

- Owner preference for five filings a year instead of twenty-five — predictable, formula-driven tax.

When Composition is the Wrong Call

- Any B2B revenue — corporate buyers cannot claim ITC against a composition invoice.

- Exporters or planned inter-state sellers — both are prohibited under composition.

- Sellers on major e-commerce marketplaces that collect TCS — categorically excluded.

- Thin-margin traders buying from 18% or 28% input chains — foregone ITC outweighs the 1% saving.

- Businesses likely to scale past the threshold within one to two years — transition cost is real.

The Break-Even Argument

Composition is cheaper than regular GST only when the effective tax saving on value-added margin exceeds the ITC forfeited on inputs. The cleaner mental model: "Is the business paying 1% of revenue, or 18% of margin? Whichever is lower wins." For most B2C retail with 25–40% margins and 5–12% input GST, composition wins comfortably. For B2B trading with 8–10% margins and 18% input GST, regular wins comfortably.

5. The Five Strategic Levers Every SME Should Review Annually

- Vendor compliance scoring. Grade the top suppliers A, B, or C by GSTR-1 filing punctuality. Renegotiate payment terms with B and C — release payment after the invoice reflects in GSTR-2B, not before. This single discipline routinely unlocks meaningful working capital that would otherwise stay blocked.

- ITC audit every September. The November cut-off for prior-year ITC is non-negotiable; September leaves a 60-day window to chase missing invoices.

- QRMP-versus-monthly review every March. Switching costs nothing but cuts paperwork substantially for the right profile.

- LUT renewal in the first week of March. A lapsed LUT silently turns export invoices into IGST-liable transactions — a costly oversight that recurs every year for export-oriented SMEs.

- Notice-readiness folder. One digital folder per FY containing invoices, e-way bills, bank statements, and reconciliations. Scrutiny and pre-show-cause windows are short; preparedness converts a crisis into a routine deliverable.

6. Where the Real Advisory Value Sits

Software can file returns. AI can draft notices. What neither can do is:

- Model whether composition or regular costs less over a three-year scaling plan.

- Flag that an LUT is about to lapse before a high-value export order goes out.

- Read a pre-show-cause notice and decide whether to litigate, reply, or settle under Section 73.

- Negotiate a scrutiny closure with the jurisdictional officer.

- Trace stuck ITC back to vendor behaviour rather than portal issues.

That is the layer worth paying for. The filing is the by-product.

Closing Note

An SME owner reading this should walk into the next consultant conversation with three questions:

- Given the current customer mix and growth plan, is the business in the right filing lane this year?

- What does the vendor compliance scoreboard look like, and which suppliers are silently costing the business ITC?

- What is the single most likely notice the business could receive in the next twelve months, and is it ready for one?

If those three cannot be answered in five minutes, the engagement is paying for filing, not for advisory. That is the gap MACS Edge exists to close.

MACS Edge | Corporate, Tax & Compliance Advisory | www.macsedge.com